Angel Investing From Scratch: The Fundamentals Every First-Time Startup Investor Needs to Know 💡

A guide to the fundamentals of how to think about investing in startups at angel stage

Angel investing looks glamorous from the outside.

In reality, it is mostly uncertainty, pattern recognition, and disciplined patience.

At this stage, you do not have enough information to be “certain.”

You are not underwriting a mature business.

You are backing a team, a market, and a set of hypotheses that may or may not become a real company.

That is why the best angel investors do not start with excitement.

They start with risk.

If you are evaluating startups at the angel stage, the real task is not to predict the future perfectly.

It is to identify:

where the risk lives,

which risks are fatal,

which risks are acceptable,

and whether the upside is large enough to justify the bet.

Frontier Deal Flow 🎯

Companies struggle to reach the right investors. Investors struggle to find signal.

Frontier Deal Flow is a monthly curated database by 22nd Century Frontier, connecting high-quality companies with thousands of:

Angel investors, VC funds, corporate venture capital arms, venture syndicates, private equity firms, family offices, institutional investors, strategic corporate partners, and more.

Why submit:

• Get in front of serious investors actively looking for opportunities

• Share your raise in a clear, high-signal format

• Skip cold outreach

Submissions are completely FREE. For the March & April issue, submissions close 30 April, and the report goes live 1 May.

Key Takeaways

Angel investing starts with risk, not excitement

The best angels look for failure modes first and only invest when the upside clearly justifies the uncertainty.A clear thesis matters more than a gut feeling

Every check should be tied to a specific belief about the team, problem, market, and timing.Knowns and unknowns help you think clearly

Separate what is verifiable now from what still needs to be proven, then decide whether the remaining risk is worth underwriting.Fast rejection is a skill, not a weakness

Saying no early to obvious mismatches saves time and creates room for the small number of deals that deserve deeper attention.Angel investing works best as a portfolio game

Diversification, follow-on reserves, and clean deal structure matter because the returns are driven by a few outliers, not every deal.

Table of Contents

1. Start With The Risk First

The first habit to build is simple:

Assume most ideas will not work.

That is not pessimism.

That is the correct default.

Angel investing improves when you ask, very early:

What would make this company fail?

Maybe the problem is too weak.

Maybe the market is too small.

Maybe the team is not aligned.

Maybe the product needs a distribution channel that will cost too much to buy.

Maybe the unit economics never recover.

The point is to identify the failure mode before you fall in love.

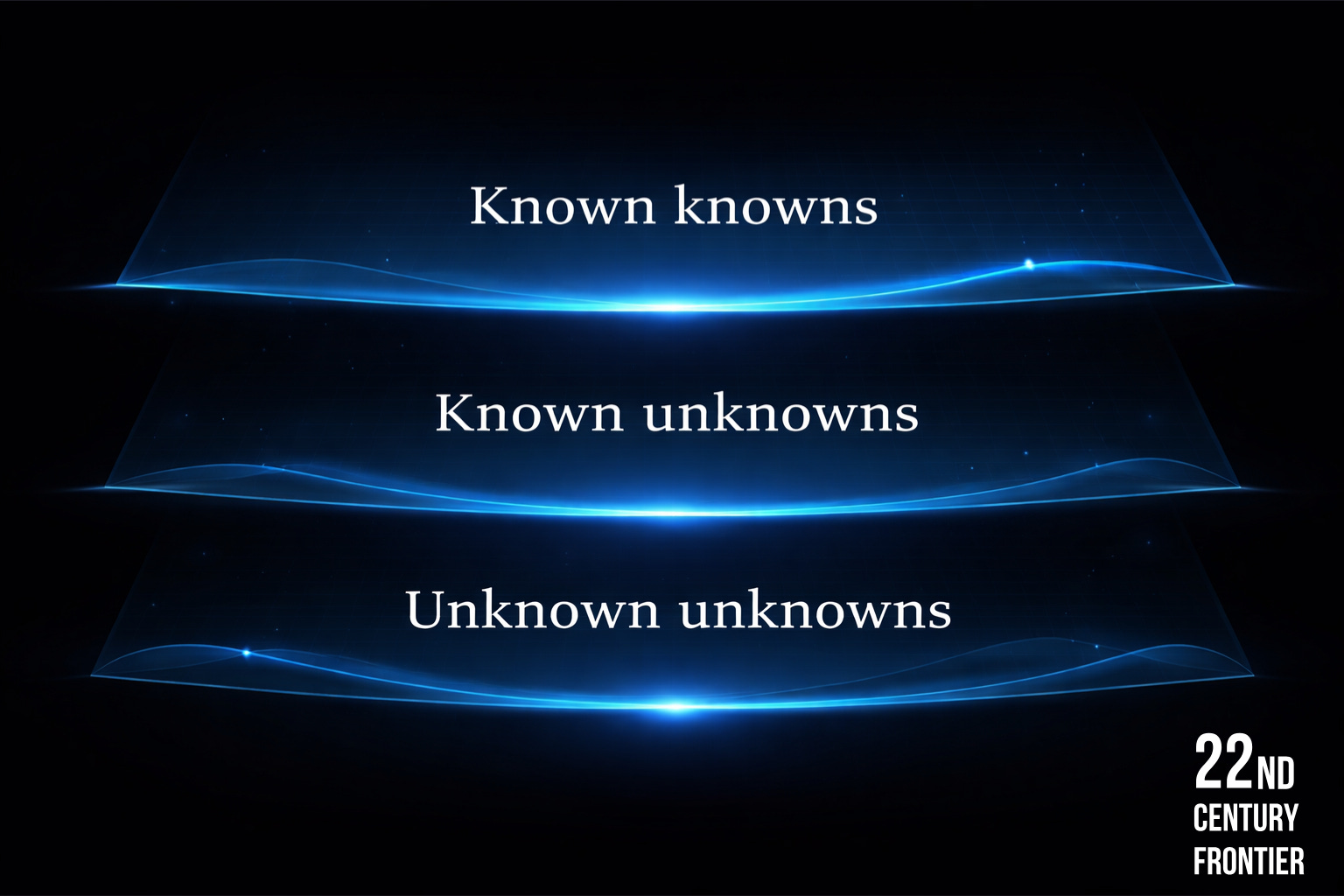

2. Use A Knowns And Unknowns Map

Angel investing lives in uncertainty, so it helps to sort information into buckets.

One way to make this practical is to use structured prompts that force you to separate assumptions from facts and surface the most important unknowns early.

Known knowns are the facts you can verify now:

who the founders are

what problem they claim to solve

what traction they already have

where they operate

what stage they are raising

Known unknowns are the questions that matter but are not yet answered:

can this team actually execute?

will customers keep paying?

will acquisition cost rise too quickly?

is the market truly large enough?

can this product become a category, not just a feature?

Unknown unknowns are the surprises you cannot model directly:

macro shifts

regulatory change

a stronger competitor emerging

a founder leaving

a distribution channel dying

You cannot remove unknown unknowns completely.

But you can reduce exposure by building a diversified portfolio and avoiding deals that depend on fragile assumptions.

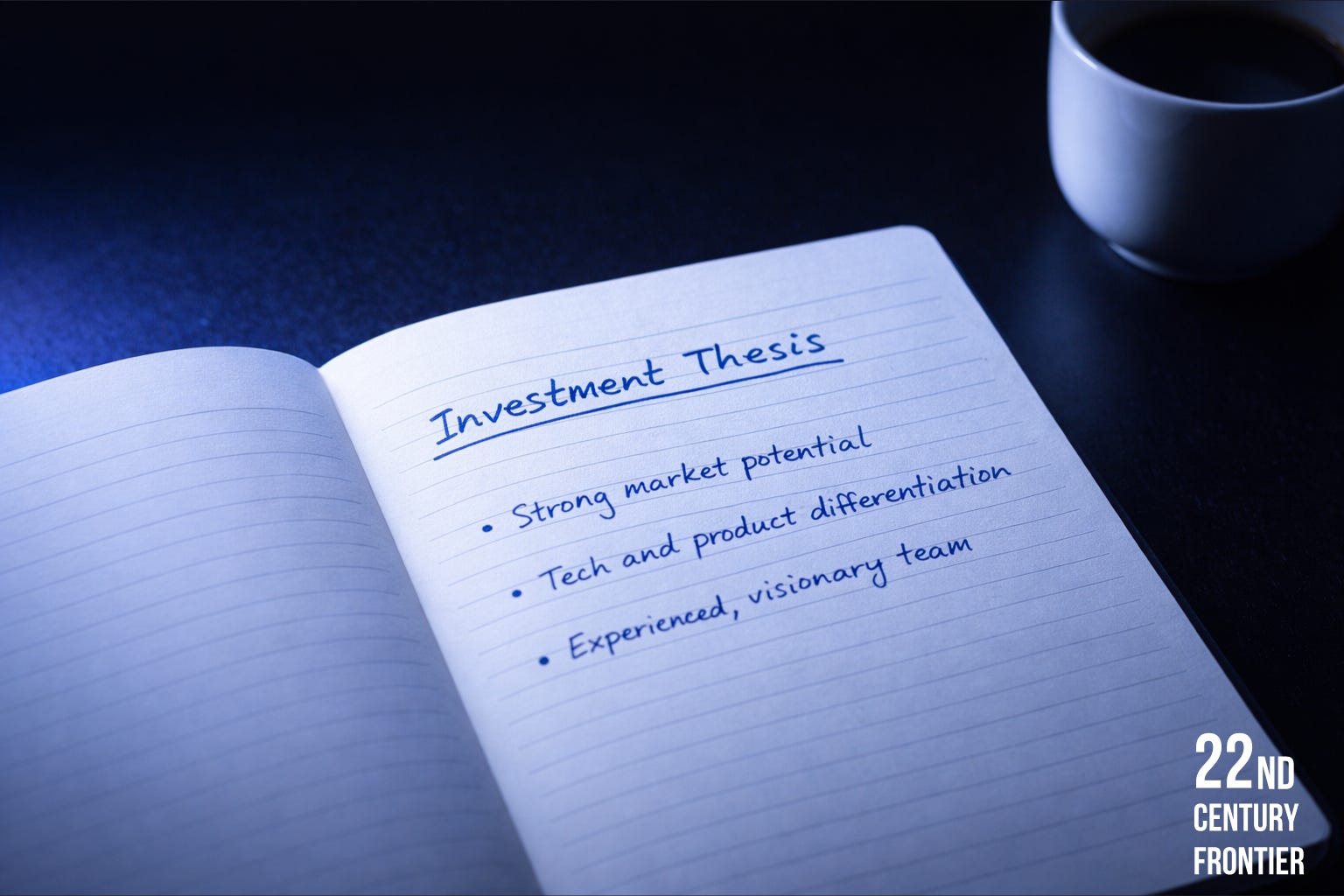

3. Write The Investment Thesis Before You Write The Cheque

Every angel investment should have a thesis.

Not a vibe.

Not a hunch.

A thesis.

Your thesis should answer:

Why this team?

Why this problem?

Why now?

Why this market?

Why is this likely to become much bigger than it looks today?

A good thesis forces you to say what has to be true for the company to work.

Example:

A founder building software for independent dental clinics may look small on paper.But if your thesis is that clinic software adoption is still fragmented, that the founder understands the workflow deeply, and that expansion into adjacent practice-management workflows is plausible, the deal may make sense.

Without a thesis, you are just collecting pitches.

4. Learn To Reject Quickly And Politely

Not every startup deserves deep analysis.

In angel investing, speed matters.

If a business is:

clearly outside your focus,

too early,

too capital-intensive,

or missing a basic ingredient,

say no early.

The faster you filter, the more energy you reserve for the few deals that actually deserve attention.

A few examples:

A consumer hardware startup with no clear distribution plan

A biotech idea with no technical edge and no access to the science

A marketplace that needs liquidity in three countries on day one

A founder who cannot explain the customer in one sentence

A good no protects your time, your reputation, and your capital.

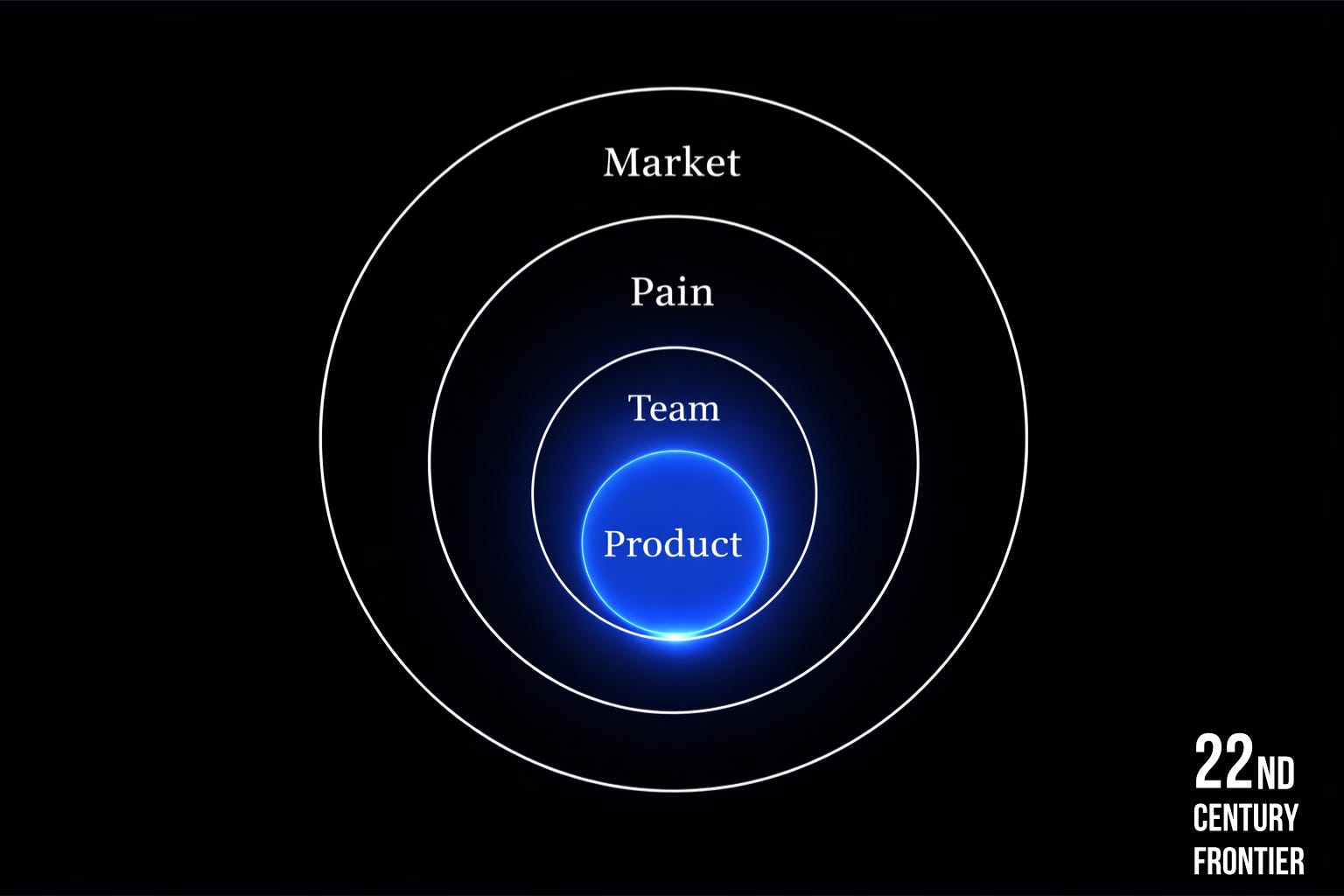

5. Market First, Team Second, Product Third

People love to say “bet on the jockey.”

That is only partly true.

A great team in a bad market can still lose.

A decent team in a strong market can win if the timing is right and the product solves a painful problem.

The order I like is:

Is the market real?

Is the pain urgent?

Is the team capable?

Is the product a credible answer?

Is the timing favorable?

For angel investors, the key is not perfection.

It is directional truth.

A company building software for compliance-heavy industries, for example, might have slower sales cycles but stronger retention if the product becomes embedded. That changes the bar for what “good” looks like.

6. Unit Economics Are A Compass, Not A Trophy

At angel stage, you will not know everything about unit economics.

But you should absolutely know enough to judge direction.

You want early signals on:

how customers are acquired

what they are worth over time

how quickly the company recovers acquisition cost

If the business model only works with unrealistic assumptions, it is not a business model.

It is hope.

You do not need perfect data.

You need directional logic.

A subscription tool for small accounting firms can look very attractive if:

acquisition is low-cost through referrals or niche communities

churn is low

customers stay long enough to create durable value

The point is not to finalize the spreadsheet.

The point is to know whether the spreadsheet is pointing toward something real.

7. Portfolio Thinking Matters More Than Hero Thinking

Angel investing is a portfolio game.

One company can do everything right and still fail.

Another can look messy and still become enormous.

That is why concentration in a few names is dangerous.

A sensible angel portfolio usually includes enough independent bets that one or two breakout winners can carry the rest of the book.

The exact number depends on your budget, access, and risk tolerance, but the logic is the same:

Outcomes are uneven.

Also, reserve capital for follow-on.

If one of your early checks starts showing real traction, you want the ability to support it again.

Your best returns rarely come from the first cheque alone.

They come from backing your winners when the signal becomes clearer.

8. Deal Structure Should Not Sabotage The Upside

Good deals can be ruined by sloppy structure.

As an angel, you want simplicity:

clean terms

understandable economics

no unnecessary complexity

enough room for later investors to join comfortably

If the early round is structured in a way that frightens future investors or over-dilutes the founder, you may damage the company you are trying to support.

A founder who feels crushed by the cap table is not a better founder.

They are just more constrained.

Keep it fair.

Keep it readable.

Keep it compatible with the next round.

9. The Best Angels Create Optionality

The real value of an angel investor is not only capital.

It is judgment, access, and pattern recognition.

Good angels help founders:

avoid obvious mistakes

meet the right people

refine their raise

understand what downstream investors will care about

That means you should think like a future investor from day one.

What will the seed investor ask?

What proof will they need?

What needs to be true for the company to move to the next stage?

If you understand that, you stop betting blindly and start underwriting progress.

10. Final Thought

Angel investing is not about trying to be right on every deal.

It is about knowing what you can know, naming what you cannot, and backing a small number of founders whose upside justifies the risk.

Use a risk-first mindset.

Write a thesis.

Filter fast.

Support winners.

Structure cleanly.

Think in portfolios, not fantasy exits.

That is how you get better at angel investing without confusing luck for skill.

Continue Exploring the Frontier

If this piece resonated, you may want to go deeper.

Here are three recent articles readers found especially useful:

Each one tackles a different part of the same challenge: building with intent, not hope.

If you are serious about shaping the future rather than reacting to it, you are exactly where you should be.

WHY SUBSCRIBE | PREMIUM RESOURCES | ENTERPRISE PLAN | ADVERTISE

The hardest part is access to the best founders and getting into their cap tables IMHO. Doing they in enough volume

Angel investing is *a whole new world* (cue the Disney song)

That Iceberg vvisual is pretty useful.